Michael Gofman

Senior Lecturer in Finance at the Hebrew University of Jerusalem

Research Interests: Financial Networks, Financial Intermediation, Financial Regulation, Production Networks, Trade Credit, Systemic Risk, Financial Stability, Payment Systems, Creative Destruction, Artificial Intelligence, Director Networks, SPACs

Curriculum VitaeContact Information:

Follow @michaelgofman |

Working papers

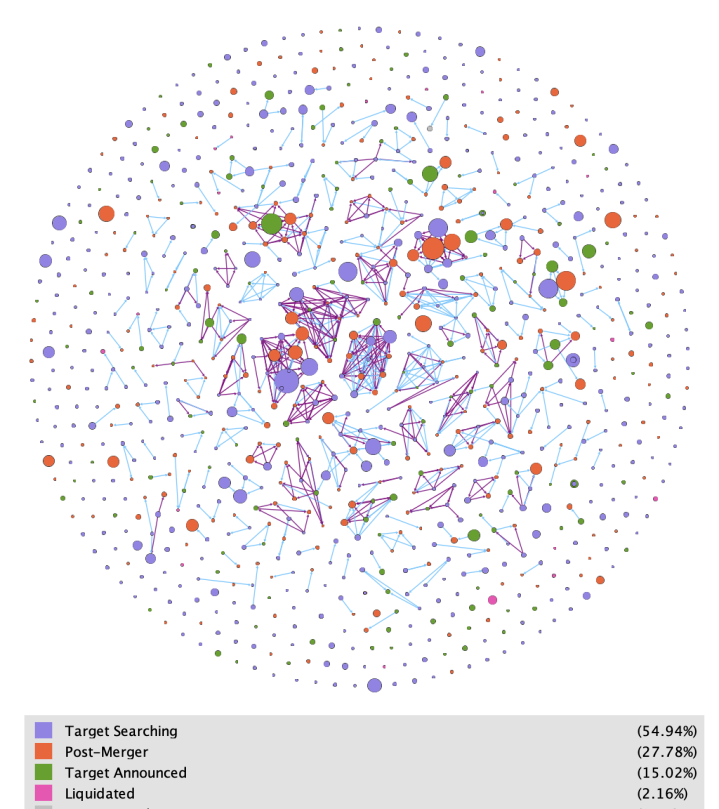

SPACs' Directors Network: Conflicts of Interest, Compensation, and Competition with Yuchi Yao In 2010-2021, 972 SPACs raised $271 billion and hired 4,056 directors to facilitate mergers with private firms. We show theoretically and empirically that entrant SPACs inefficiently front-run the deal flow by hiring incumbent SPACs' directors. Incumbent SPAC's lower compensation and longer time to liquidation decrease directors' compensation from the entrant SPAC but increase the chance for the conflict of interest to emerge. Empirically, higher pay by the entrant SPAC increases the chance that a director misallocates the target, hurting the returns of the incumbent SPAC's investors. Our welfare analysis provides conditions when banning concurrent SPACs' board membership is desirable.

|

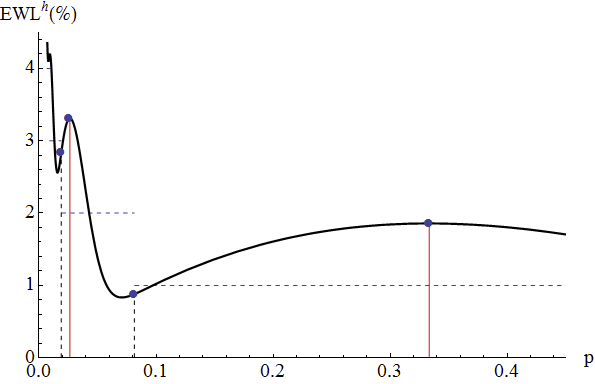

A Network-Based Analysis of Over-the-Counter Markets (R&R Review of Financial Studies) I study how intermediation in over-the-counter markets affects their allocational efficiency. Over-the-counter markets are modeled as a trading network in which bilateral prices and trading decisions are jointly determined in equilibrium. Market efficiency depends crucially on the network structure and the split of surplus between traders. The probability that market allocations are always efficient tends to zero in large markets. The expected welfare loss can be substantial and it can increase even if the amount of intermediation decreases. A large interconnected financial institution can improve efficiency. This welfare gain should be considered when deciding whether large financial institutions are too-interconnected-to-exist.

|

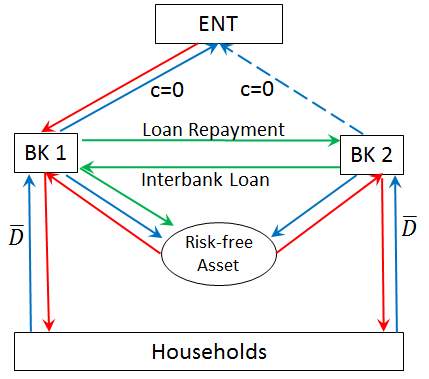

Commit not to Compete: Collusion versus Liquidity Sharing via Interbank Markets with Dean Corbae We provide a simple theoretical framework and show empirically that interbank markets can provide a channel for banks to collude in the market for business loans. By lending funds in the interbank market to a competitor, a bank commits not to compete in the private loan market. Interbank interest rates allow banks to split the benefits from such collusion. Using global syndicated loans data, we show that firms paid 31bps higher spread on $239 billion of loans provided by banks that took an interbank loan from a competitor. Our findings have important implications for the regulation of interbank markets.

|

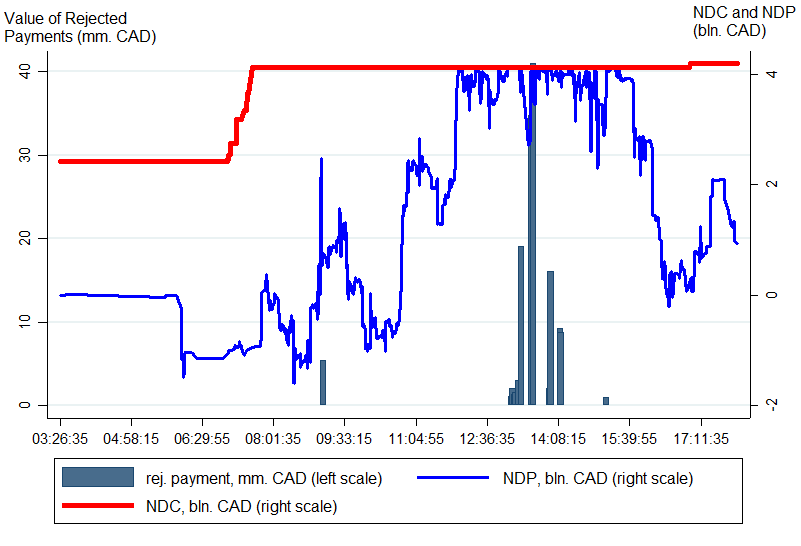

High-frequency analysis of financial stability with James Chapman and Sajjad Jafri We utilize 500 trillion CAD of interbank payments to compute high-frequency measures of systemic risk in Canadian Large Value Transfer System (LVTS). We find that banks started to delay provision of bilateral credit limits in the second half of 2005. During 2007-2009, LVTS experienced an abnormal increase in delayed and rejected payments due to binding collateral and credit constraints. Bank of Canada's injection of liquidity in 2008-2010 relaxed collateral constraints and reduced systemic risk in LVTS. Overall, our high-frequency risk measures help to identify vulnerabilities caused by the fundamental efficiency-stability trade-off in the design of payment systems.

|

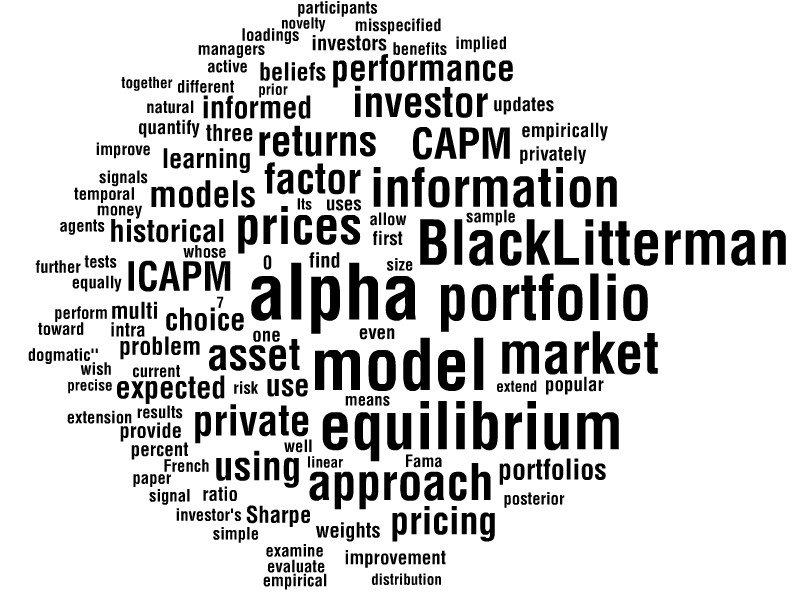

An Empirical Evaluation of the Black-Litterman Approach to Portfolio Choice with Asaf Manela We evaluate the Black-Litterman equilibrium model approach to portfolio choice. We quantify the improvement in portfolio performance of a privately informed investor who learns from market prices over an equally informed, but dogmatic investor who only uses private information. We extend the approach to any linear multi-factor asset pricing model (e.g. ICAPM) to examine how learning from prices using different equilibrium models affects portfolio performance. We find that even a misspecified asset-pricing model can improve portfolio performance when private signals are not extremely precise. As we increase the noise in private information, learning from prices is initially harmful and gradually becomes more beneficial.

|

Published papers

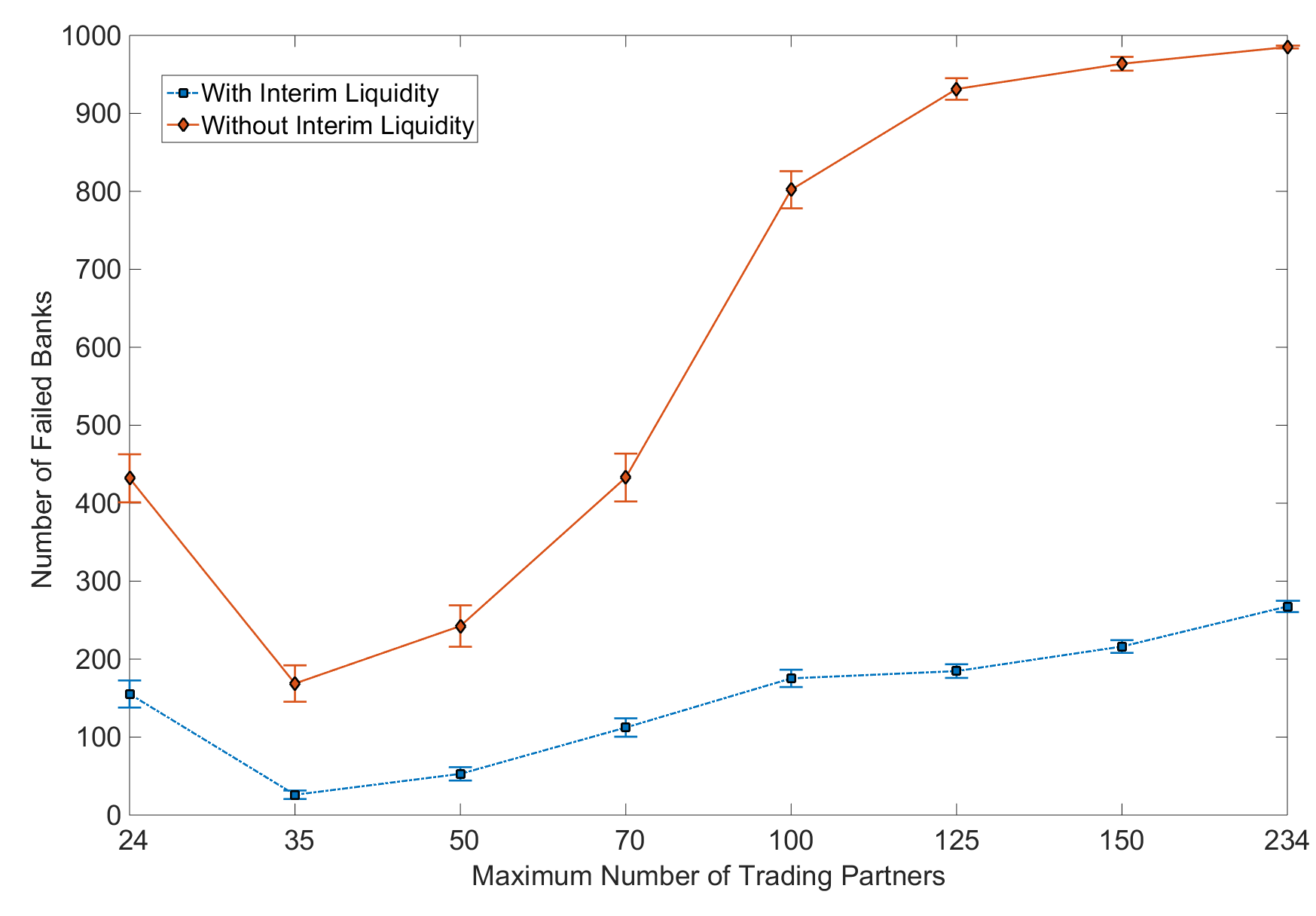

Efficiency and Stability of a Financial Architecture with Too-Interconnected-To-Fail Institutions (Journal of Financial Economics, 2017, Vol 124, Issue 1) The regulation of large interconnected financial institutions has become a key policy issue. To improve financial stability, regulators have proposed to limit banks' size and interconnectedness. I estimate a network-based model of the over-the-counter interbank lending market in US and quantify the efficiency-stability implications of this policy. Trading efficiency decreases with limits on interconnectedness because the intermediation chains become longer. While restricting the interconnectedness of banks improves stability, the effect is non-monotonic. Stability also improves with higher liquidity requirements, when banks have access to liquidity during the crisis, and when failed banks' depositors maintain confidence in the banking system.

|

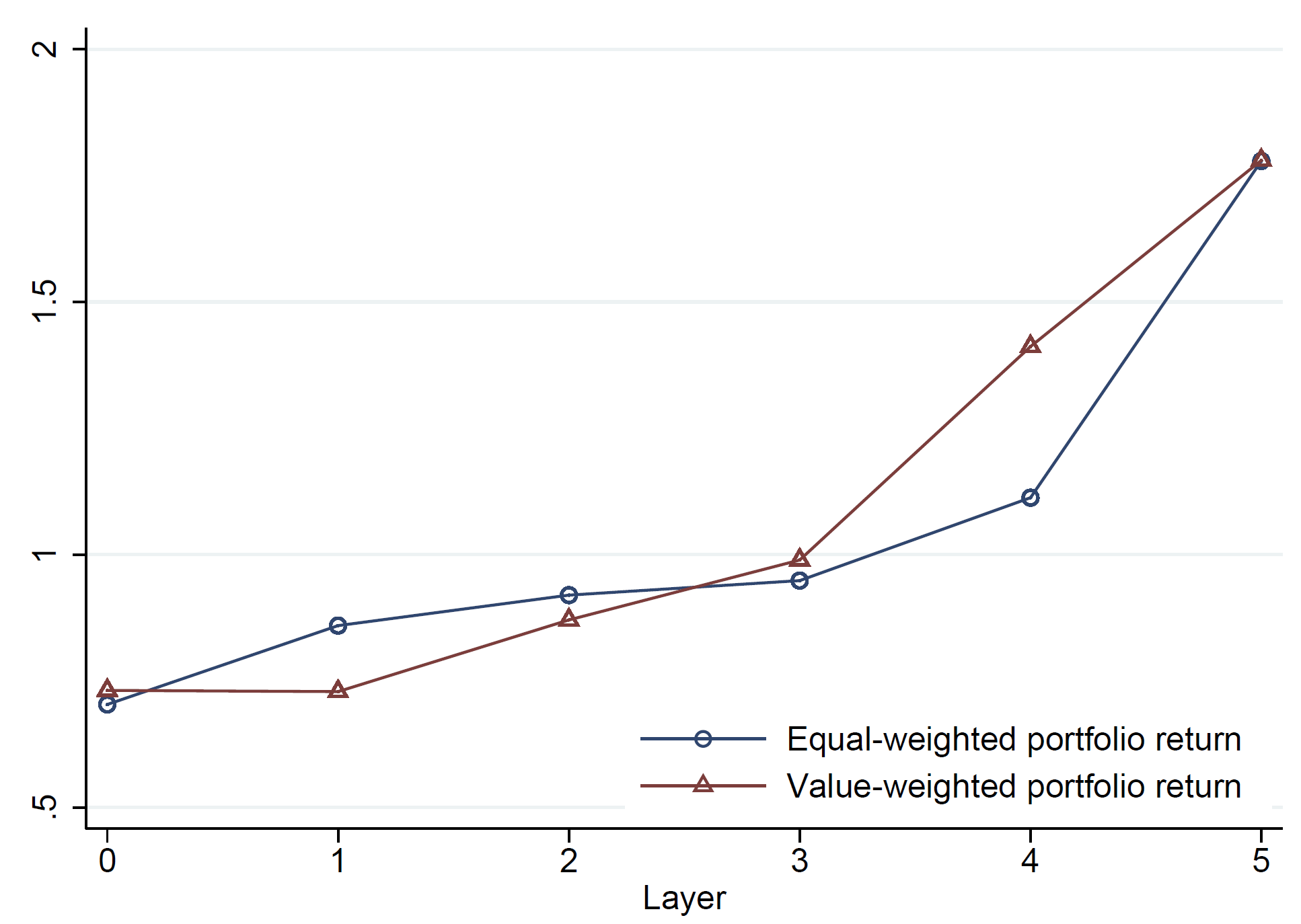

Production Networks and Stock Returns: The Role of Vertical Creative Destruction with Gill Segal and Youchang Wu (Review of Financial Studies, 2020, Vol 33, Issue 12) We study the relation between firms' risk and their upstreamness in a production network. Empirically, firms' average stock returns and aggregate productivity exposures increase monotonically with their upstreamness. We quantitatively explain these novel facts using a multi-layer general equilibrium model. These patterns arise from vertical creative destruction - innovations by suppliers devalue customers’ assets-in-place. We confirm several model predictions, and document additional new facts consistent with vertical creative destruction: a diminished value premium among downstream firms and a negative relation between downstream firms’ returns and their suppliers’ competitiveness. Overall, vertical creative destruction has a sizable effect on cross-sectional risk premia.

|

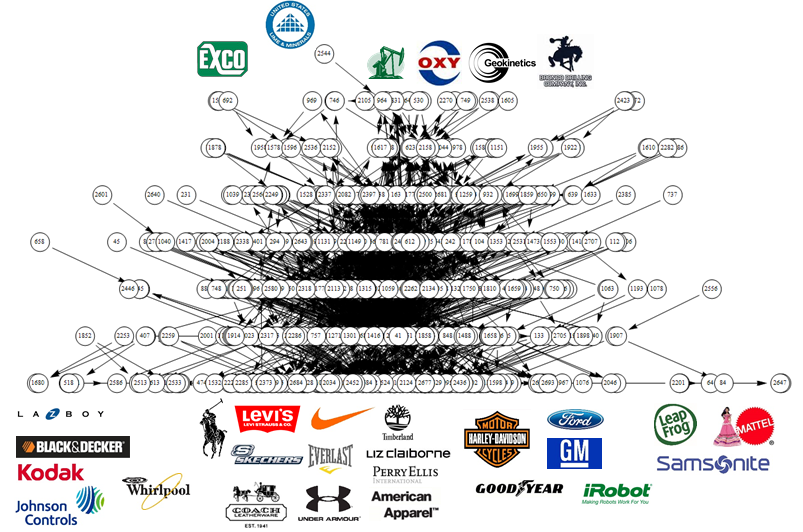

Trade Credit and Profitability in Production Networks with Youchang Wu (Journal of Financial Economics, 2022, Volume 143, Issue 1) We construct a sample of over 200,000 supply chains to conduct a chain-based analysis of trade credit. Our study uncovers novel stylized facts about trade credit both within and across supply chains. More upstream firms borrow more from suppliers, lend more to customers, and hold more net trade credit. This upstreamness effect in trade credit is weaker for more profitable firms and for longer chains. Firms in more central or more profitable chains provide more net trade credit. Our results are generally consistent with the recursive moral hazard theory of trade credit. Evidence for the financing advantage theory is mixed.

|

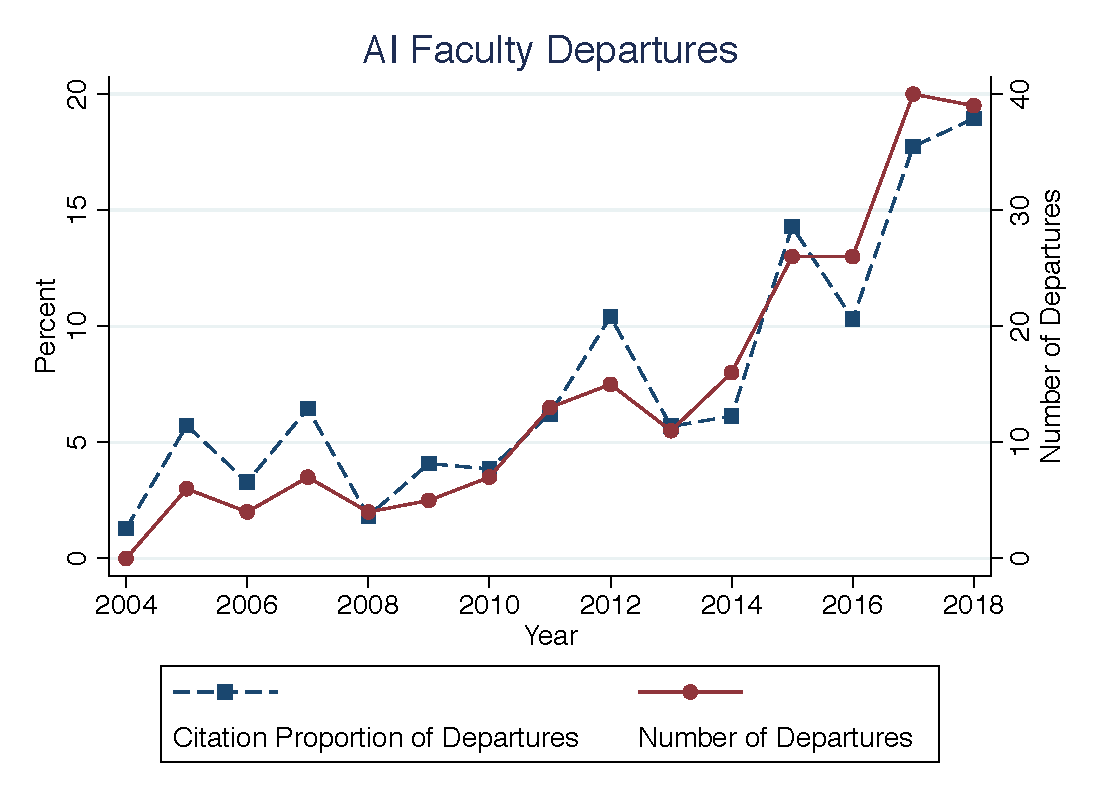

Artificial Intelligence, Education, and Entrepreneurship with Zhao Jin (Journal of Finance, Forthcoming) We document an unprecedented brain drain of AI professors from universities from 2004 to 2018. We find that students from the affected universities establish fewer AI startups and raise less funding. The effect is significant for an AI brain drain of tenured professors, professors from top universities, and deep learning professors. Additional evidence suggests that unobserved city- and university-level shocks are unlikely to drive our results. We consider several economic channels for the findings. The most consistent explanation is that professors' departures reduce startup founders' AI knowledge, which we find is an important factor for successful startup formation and fundraising.

|